30‑Second Takeaway

Adding a child to your deed does avoid probate—but it also hands your house to their creditors, ex‑spouse, and the IRS, and it can even delay Medicaid benefits. Better tools—like a Florida Lady Bird Deed or a simple revocable trust—pass the home with none of those headaches.

Let’s say you’re getting older. (We all are, right?) And you’re concerned about passing on your home to your children.

Should you put your children’s names on the deed to your home?

Many people add their children’s names to their bank accounts, especially as they get older, so their children can help them pay their bills and manage their finances if it becomes too difficult.

Some people add their children’s names to the deed to the family home as a “do‑it‑yourself” estate‑planning technique.

Bad idea.

It is a bad idea to try to do your estate planning yourself and to add your children’s names to the deed to your home. Working with an experienced estate‑planning attorney is essential to reviewing your assets and devising an appropriate estate plan, including passing your home.

Two Hats, Two Very Different Rulebooks

| Option | Who Controls the House Today? | Who Gets It at Your Death? | What Could Go Wrong? |

|---|---|---|---|

| Add Child to the Deed (Joint Tenants / Tenants-in-Common) | You and Child must sign off on any sale or refi | Child takes full title immediately—probate avoided | Loss of control, creditor/divorce risk, loss of tax “step-up,” Medicaid penalty |

| Keep Deed in Your Name + Use a Revocable Trust or Lady Bird Deed | You keep 100% control | Trust beneficiary or “remainderman” gets house—also probate-free | Must draft documents correctly (we can help!) |

(See our deep dive on the Lady Bird Deed vs. Trust for pros and cons.)

The Complications Are Many

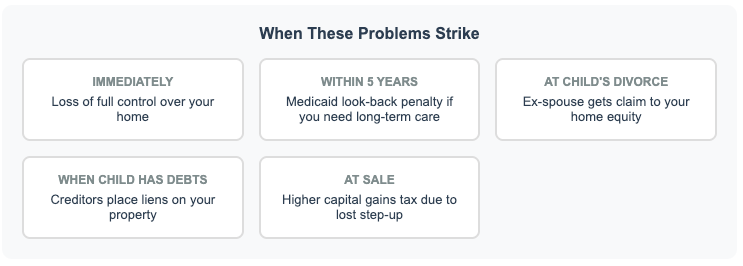

Putting your children’s names on the deed to your home can have any number of negative consequences, two of which we will discuss in more detail below.

Many times, people add their children’s names to the deed of the family home to avoid probate or prevent the family home from being sold to pay for nursing home expenses. But this can lead to unfortunate consequences.

First, understand that when you put your children’s names on the deed to your home, you are giving them an interest in your real property. The type of deed you use matters significantly. Understanding the different types of deeds in Florida can help you see why some transfers create more risk than others. Once you add them to the deed, they now become co‑owners with you in your home. This means they, like you, have the legal right to sell, devise, or encumber (take out a loan) their interest in your home. It also means that if you want to sell your home, you must get your children, as co‑owners, to agree.

Now, think about this. What if the child whose name you put on the deed to your home is married? He (or she) can give, sell, or bequeath his share in your home to his spouse. Want that?

Or, what happens if your married child divorces? Because Florida is an equitable‑distribution state, if your child acquired title to the home during the marriage, the co‑ownership interest in your home will be marital property subject to equitable division by the family law courts. In other words, your daughter‑in‑law or son‑in‑law could be awarded half of your child’s interest in your home as part of the divorce.

Now think about this: studies place the lifetime divorce risk for first marriages at roughly 35–40 %, so even a well-intentioned gift of home equity can wind up inside a property-division battle. (USAttorneys.com. “Divorce Statistics in 2024: Trends & Insights.”)

Another way you could end up co‑owning your home with your daughter‑in‑law, son‑in‑law, or a complete stranger is if your child whose name is on the deed dies and leaves their interest to their spouse or a friend.

Putting your children’s names on the deed to your home can also lead to tax complications. Briefly, when you put your child’s name on your deed, for tax purposes, they will be considered to have acquired their portion of the home at the same price you paid for the house. If, at the time of your death, your child sells the home, he or she will have to pay capital‑gains tax on the part of the home they acquired before your death.

Depending on how much equity you have in your home, the capital‑gains tax consequences for your child could be considerable. In contrast, if your child does not inherit his/her portion of the home until after your death, they take the home based on the date‑of‑death value, which in almost all cases is going to be far closer to the current market value than what you originally paid for the home. Then, when they go to sell it, there will be no capital‑gains tax.

These are just some of the negative consequences of putting your children’s names on the deed to your home. There are others.

Five More Pitfalls Florida Homeowners Overlook

And there’s more… Here are five hidden pitfalls we see every month in Florida closings:

- Loss of control – Every refinance or HELOC now needs your child’s signature.

- Divorce drama – A national divorce rate of 2.4 per 1,000 means your in‑law could end up on the title. (CDC)

- Creditor & lawsuit liens – Co‑ownership can pierce homestead protection if the child’s judgment attaches. (The Florida Bar)

- Gift‑tax paperwork – Transferring more than the $19,000 annual exclusion (2025) forces an IRS Form 709. (IRS)

- Step‑up in basis lost – Your original low basis carries over; no full “step‑up” at death, meaning tens of thousands in capital‑gains tax. (IRS)

There Are Additional Reasons Why You Should Not Put Your Children’s Names on the Deed to Your Home

1. Creditor’s Claims

As noted above, when you put your children’s names on the deed to your home, you give them a legal interest in it. That comes with responsibilities and privileges. One of the privileges we mentioned above is that your child now has the legal right to encumber his/her interest. That means he can take out a loan and use his interest in your home as collateral.

It also means that if your children have unpaid debts, their creditors can use your home to collect on the debt. Your child may have credit‑card debt, unpaid loans, or may have liability from lawsuits or accidents. The point here is that if their name is on the deed to your home, you may end up paying for these debts with your home. Creditors can put a lien against your house, preventing you from selling or refinancing your home until that lien is paid off. (The Florida Bar)

2. Medicaid’s Look‑Back

One reason older people add their children’s names to the deed on the family home is that they believe it will prevent Medicaid from taking the home to pay for nursing care. They think that by getting title to the home out of their names, Medicaid won’t know that they have a house that could be used to pay for their care.

But this is an ill‑advised approach to providing long‑term health care.

Medicaid has a 5‑year “look‑back” procedure under federal law—any transfer of assets within 60 months for less than fair value can trigger a penalty period.

There are proper ways to structure your assets that do not involve putting your children’s names on your deed and do not violate Medicaid’s 5‑year look‑back rule. To learn more about this, contact us.

Whatever your estate‑planning needs are, it is always a good idea to consult an experienced estate‑planning lawyer near you before you do anything to get the help and advice you need.

Smarter, Low‑Drama Alternatives

| Tool | Why We Like It | Need-to-Know |

|---|---|---|

| Enhanced Life Estate (Lady Bird) Deed | Avoids probate and you keep full control | Re-sign loan docs if you refinance after recording |

| Revocable Living Trust | Keeps all kids equal, bundles multiple assets | Home must be retitled into the trust |

| Limited Durable POA + Trust | Lets a child help with finances without owning the house | POA ends at death—trust handles transfer |

| Transfer-on-Death (TOD) Deed | Great for out-of-state property in TOD-friendly states | Not available for Florida real estate |

Curious which route fits you? Grab our free guide: 5 Strategies to Avoid Probate in Florida.

Quick FAQ (Plain English)

Does adding my child protect the house from Medicaid?

No. Medicaid still sees the transfer during its 5‑year look‑back. (Medicaid Planning Assistance)

Will I owe gift tax right away?

Unlikely, but any gift of ≥ $19,000 in 2025 requires IRS Form 709. (IRS)

Isn’t probate expensive?

Yes—use a Lady Bird Deed or trust to avoid it without the extra risks.

What if I already put my child on the deed?

A corrective deed or trust transfer may fix it. Call us before acting.

Next Steps & How We Can Help

Adding a child to your deed is quick; fixing the fallout isn’t. Let’s design a plan that protects both your roof and your relationships.

Call 954‑580‑3690 or schedule a consult—virtual statewide and in‑person across South Florida.