How to Protect Your Spouse and Guarantee Your Children’s Inheritance

Blended families face one of the most difficult challenges in estate planning:

How do you take care of your spouse without accidentally disinheriting your children?

It’s a real and common risk. Without the right legal structure, assets left to a surviving spouse can later be redirected, intentionally or unintentionally, leaving your children with nothing.

The good news is that you don’t have to choose between your spouse and your children.

There is a proven estate planning solution designed specifically for this situation.

Watch the Video: Best Trust for Blended Families

In this video, you’ll learn:

- The biggest estate planning risk for blended families

- How a QTIP trust works

- How to protect both your spouse and your children

- Alternative trust strategies to consider

Quick Answer

The best trust for most blended families is a QTIP Trust (Qualified Terminable Interest Property Trust).

It allows you to:

- Provide income and support to your spouse for life

- Lock in your children as the ultimate beneficiaries

- Prevent changes to your estate plan after your death

The Core Problem in Blended Family Estate Planning

When you remarry, your existing estate plan can quickly become outdated.

Common Scenario

You leave everything to your spouse in a will.

But later:

- Your spouse remarries

- Updates their estate plan

- Redirects assets elsewhere

Result

Your children may receive nothing.

Key Issue

Florida law does not automatically protect stepchildren.

Without a clear plan, your intentions may not be honored.

Why a Will Alone Is Not Enough

Many people rely on a will for simplicity, but for blended families, this can create risk.

A will:

- Transfers assets to your spouse

- Gives them full control

- Does not guarantee what happens next

This means your entire legacy depends on future decisions you cannot control.

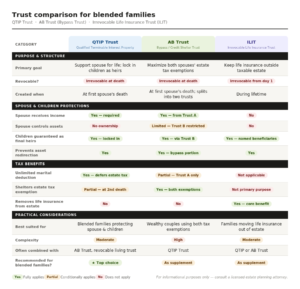

The Solution: QTIP Trust (Qualified Terminable Interest Property Trust)

A QTIP trust is specifically designed to solve this problem.

How It Works

Think of it as a two-stage inheritance plan:

Step 1: Support for Your Spouse

After your death:

- Your spouse receives income from the trust

- This may include:

- Interest

- Dividends

- Rental income

They are financially supported for life.

Step 2: Protection for Your Children

Your spouse:

- Does NOT own the trust assets

- Cannot change beneficiaries

- Cannot redirect the inheritance

After your spouse passes away:

- The remaining assets go directly to your children

Exactly as you intended.

Why QTIP Trusts Work So Well

A QTIP trust creates balance:

For Your Spouse

- Lifetime financial security

- Stable income

- Protection without full ownership

For Your Children

- Guaranteed inheritance

- Protection from changes or disputes

- Clear, enforceable structure

This makes it one of the most effective tools for blended families.

Tax Benefits of a QTIP Trust

QTIP trusts also offer important tax advantages.

Unlimited Marital Deduction

- No estate tax is due when the first spouse dies

- Taxes are deferred until the second spouse’s death

2026 Estate Tax Exemption

- $15 million per person

- $30 million per married couple

Additional Benefits

- Potential tax-deferred growth

- Avoidance of probate

- Efficient wealth transfer

Even if your estate is below the exemption, these benefits can still be valuable.

Alternative Trust Options to Consider

While QTIP trusts are often the best solution, there are other strategies.

AB Trust (Bypass Trust)

An AB trust splits assets into two parts:

- One share for the surviving spouse

- One share locked in for children

Pros

- Uses estate tax exemptions

- Provides flexibility

Cons

- More complex

- Less direct control compared to QTIP

Irrevocable Life Insurance Trust (ILIT)

An ILIT holds a life insurance policy for your children.

Benefits

- Tax-free inheritance

- Immediate liquidity for children

- Separate from spouse-controlled assets

Use Case

Often combined with a QTIP trust for a balanced strategy.

The Missing Piece: Communication

Even the best legal plan can fail without clear communication.

What You Should Do

- Talk openly with your spouse

- Explain your intentions

- Align on what “fair” looks like

This is not about distrust—it’s about clarity.

Clear communication helps prevent:

- Family conflict

- Misunderstandings

- Future disputes

Key Takeaways

- Blended families face unique estate planning risks

- A will alone is often not enough

- A QTIP trust protects both spouse and children

- It ensures lifetime support and guaranteed inheritance

- Proper planning prevents conflict and unintended outcomes

When to Speak With an Estate Planning Attorney

Blended family planning requires precision. Small mistakes can completely change how your estate is distributed.

At SJF Law Group, our attorneys bring advanced degrees and deep tax expertise to help families:

- Structure QTIP and trust-based plans

- Protect children’s inheritance

- Navigate complex family dynamics

- Optimize tax and asset protection strategies

If you’re part of a blended family, the right plan can provide long-term security and peace of mind.

Schedule a consultation today to build a plan that protects everyone you love.

Frequently Asked Questions (FAQ)

1. What is a QTIP trust?

A QTIP trust provides income to a surviving spouse while preserving the remaining assets for children or other beneficiaries.

2. Is a QTIP trust only for wealthy families?

No. It’s useful for any blended family that wants to protect children’s inheritance.

3. Can my spouse change the beneficiaries in a QTIP trust?

No. The beneficiaries are locked in when the trust is created.

4. Do I still need a will if I have a trust?

Yes. A will works alongside your trust to ensure all assets are properly transferred.

5. What is the biggest risk in blended family estate planning?

Leaving everything to a spouse without a trust can result in children being unintentionally disinherited.